Working Committees

Training Committee

|

Interview to Marcelo Moreno Montiel |

| Name: | Marcelo Moreno Montiel |

| Age: | 66 years |

| Education: | MBA in INCAE Business School, Costa Rica |

| Professional career: |

|

Interviewer: How did you become interested in the insurance business? How were your beginnings in the industry? And in the surety business?

Marcelo Moreno: I started my career in December 1972 with Grupo Gran Colombiano (Bogota), and a group of Ecuadorean businessmen. Together, we founded Seguros Equinoccial S.A.

I took my first steps in the insurance area at Aseguradora Gran Colombiana, where I became specialized in reinsurance. Later I was appointed Head of Reinsurance at Seguros Equinoccial S.A.

In 1974, there was a change in the company's shareholding and I became General Manager.

In 1987, when I was President of the Asociación de Compañías de Seguros del Ecuador, and Antonio Arosemena Gómez Lince was President of the Chamber, we agreed on merging both associations into Fedeseg: "Federación de Empresas de Seguros del Ecuador" (Federation of Ecuadorean Insurance Companies).

Mr. Agustín de Vedia, from Aseguradores de Cauciones, Argentina, invited Seguros Equinoccial S.A. to join the Panamerican Surety Association. With their support as reinsurers, we started the surety bonds line and became the first company to issue performance bonds as a general line, including Bid bonds, Advance payment bonds, Performance bonds and Proper use of letter of credit.

By the time the line was authorized, the Ecuadorean legislation did not consider insurance policies as contract guarantees; only bank, mortgage and pledge guarantees were accepted.

Interviewer: Do you remember your first operation, your first policy? What problems did you have to overcome?

Marcelo Moreno: With resources coming from the oil boom in Ecuador, public contracting was promoted, especially in the road and hydroelectric areas. In 1985 the Ley de Licitaciones y Concurso de Ofertas (Bidding law) was amended to include policies issued by insurance companies to guarantee bid, performance and advance payment.

For the contractors, bonds issued by insurance companies had the following advantages:

Bonds issued by insurance companies are, therefore, more convenient for all parties involved in the process than bank guarantees.

It was a good choice vis-à-vis bank guarantees, their distinctive feature being the conditions on payment or calling. Contractors started then to notice the benefits of this instrument which somehow protected their interests.

The main obstacle came up when the new Ley de Contratación Pública (Public Contracting Law) was passed. This law regulated the calling process by means of exorbitant on demand clauses (unconditional, irrevocable and immediate payment clauses). The unconditional nature emerges after non-fulfillment has been proved and after the contract's economic and accounting settlement.

Interviewer: How did you become aware of the need to develop the surety market?

Marcelo Moreno: In showing the advantages of the policy in the local market and the fact that, in the case of calling, resources came from abroad (reinsurance) and did not affect the assets of the local financial and banking entities.

Bank guarantees had no conditions and they thus automatically became on demand guarantees; for this reason, the public sector was looking for an instrument similar to bank guarantees and consequently included the exorbitant first demand clause in the Ley de Licitaciones.

Interviewer: What did you do as a company to develop the market?

Marcelo Moreno: Given the relevance of the public sector works, insurers did not bind technical assets as banks did, since surety bond limits were determined by reinsurance capacity and not by credit line.

Interviewer: Why do you think this business tended towards on demand bonds rather than to contract bonds?

Marcelo Moreno: Surety insurance policies included conditions that represented an obstacle to the calling process as compared to bank guarantees, from the beneficiaries' point of view.

Although the Ley de Contratación Pública does not impose any restriction on the contractor or bidder as regards the submission of guarantees, even today many public entities accept only bank guarantees.

Interviewer: How did you manage to make surety bonds preferable?

Marcelo Moreno: Contractors found these guarantees more convenient than bank guarantees because of their terms and conditions and because credit limits were not affected.

Interviewer: What kind of support did you get? Which role did the Asociación de Seguros del Ecuador or others play? How did you get to the present situation?

Marcelo Moreno: In November 1984, I was in charge of the Organization Committee of the III Regional Surety Seminar, organized by the Panamerican Surety Association in Quito.

The Banks Superintendent, the General Controller, the Minister of Public Works and the associations of contractors and insurance companies attended this meeting as guests.

On that occasion, we had the honor of listening to lecturers such as Jorge Orozco Lainé and Agustín de Vedia talking about demand bonds.

In 1985, the Ley de Licitaciones y Concurso de Ofertas of Ecuador was amended and the proposals and conclusions of that Surety Seminar were taken into account.

In 1987, the State General Controller requested PASA's advise so that, based on the discussions which had taken place at the III Regional Surety Seminar, the first steps towards a change in the legislation then in force be taken.

In 1990, the Ley de Contratación Pública was enacted, and the bidding law then in force was abolished. That same year PASA's General Assembly was also held in Quito.

Interviewer: What trend do you foresee for Ecuador and for the Andean Region?

Marcelo Moreno: In Ecuador, surety bonds issued by specialized companies are becoming increasingly important as the use of bank guarantees decreases.

Interviewed by Adriana Alvarez, Seguros Oriente, Quito, Ecuador. May 2011

CONDENSED AND CONSOLIDATED STATEMENT OF CONDITION

PRIVATE BANKING SYSTEM

EVOLUTION OF CONTINGENT ACCOUNTS 2000-2009

(in thousand USD)

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

BONDS AND GUARANTEES (INSURED RISK VALUE)

736,553

651,648

367,039

366,780

430,416

411,310

437,321

458,394

550,913

539,278

N/D

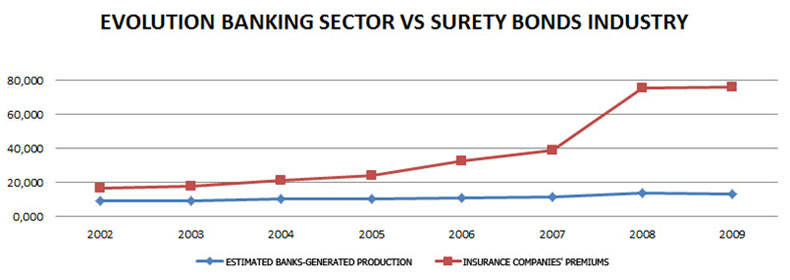

BANKS-GENERATED PRODUCTION

18,414

16,291

9,176

9,170

10,760

10,283

10,933

11,460

13,773

13,482

INSURANCE COMPANIES-GENERATED PRODUCTION

N/D

N/D

16,488

17,835

21,549

23,981

32,499

38,973

75,346

76,159

76,249

BANKS/INSURANCE COMPANIES RELATIONSHIP in %

56%

51%

50%

43%

34%

29%

18%

18%

Source: Banks Superintendence / Statistics

* Figures include an estimated commission (rate) of 2.5% per year